You open your renewal notice, look at the new premium, and say the same thing drivers all over Georgia say: “There's no way this should cost this much.”

I hear that a lot from people in Atlanta, Athens, Marietta, Macon, and every town in between. Some have clean records. Some picked up points. Some are still dealing with the fallout from a DUI or a suspension. Different stories, same problem. Car insurance keeps getting harder to afford.

The good news is you usually have more control than you think. If you want to know how to lower insurance premiums in Georgia, stop chasing gimmicks. Focus on the few moves that change how an insurer prices your risk, then clean up anything in your file that makes you look more expensive than you really are.

Why Your Georgia Car Insurance Bill Keeps Climbing

You buy a used SUV in Georgia, lock in a rate that seems fair, and move on. Then the renewal shows up higher. Same driver. Same car. Bigger bill.

That jump usually comes from one of four places. Your risk profile changed. The car costs more to repair or insure than you realized. Your record now looks worse to the carrier. Or your policy has been sitting on autopilot while rates rise around you.

Used cars catch plenty of drivers off guard. A vehicle can look clean, drive fine, and still carry baggage that affects what you pay. If you are shopping used, the insurance implications of vehicle history deserve a hard look. Prior damage, theft history, and past claims tied to that vehicle can all make an insurer price it more aggressively.

Georgia drivers with tickets, points, a suspension, or a DUI usually feel the pain fastest. Insurers do not treat those marks as old news. They treat them as a warning sign that you are more likely to cost them money. In Georgia, that makes defensive driving courses more than a box to check. A state-approved course can help some drivers reduce points for license purposes and show insurers they are taking risk seriously, which matters a lot more when your record is not spotless.

Your premium reflects how expensive the insurer believes you are likely to be.

What usually pushes a Georgia rate higher

- Your driving record changed. A speeding ticket, at-fault crash, suspension, reckless driving charge, or DUI can raise your premium fast.

- Your vehicle is pricier to insure than it appears. Repair costs, theft risk, and claim history tied to the car all affect the rate.

- You let the policy renew without checking it. Georgia drivers do this every day and pay for it.

- Your insurer sees more risk in your file than you do. That can include prior claims, coverage choices, and how long it has been since you took any step to improve your record.

Treat your premium like a quote, not a verdict. In Georgia, drivers who review the policy, use every discount they qualify for, and take a state-approved defensive driving course after a rough patch usually have the best shot at getting the bill back under control.

Review Your Policy for Quick Wins

Your renewal notice shows up. Same car. Same commute. Bigger bill. Before you shop around, clean up the policy you already have. Georgia drivers leave money on the table here every day.

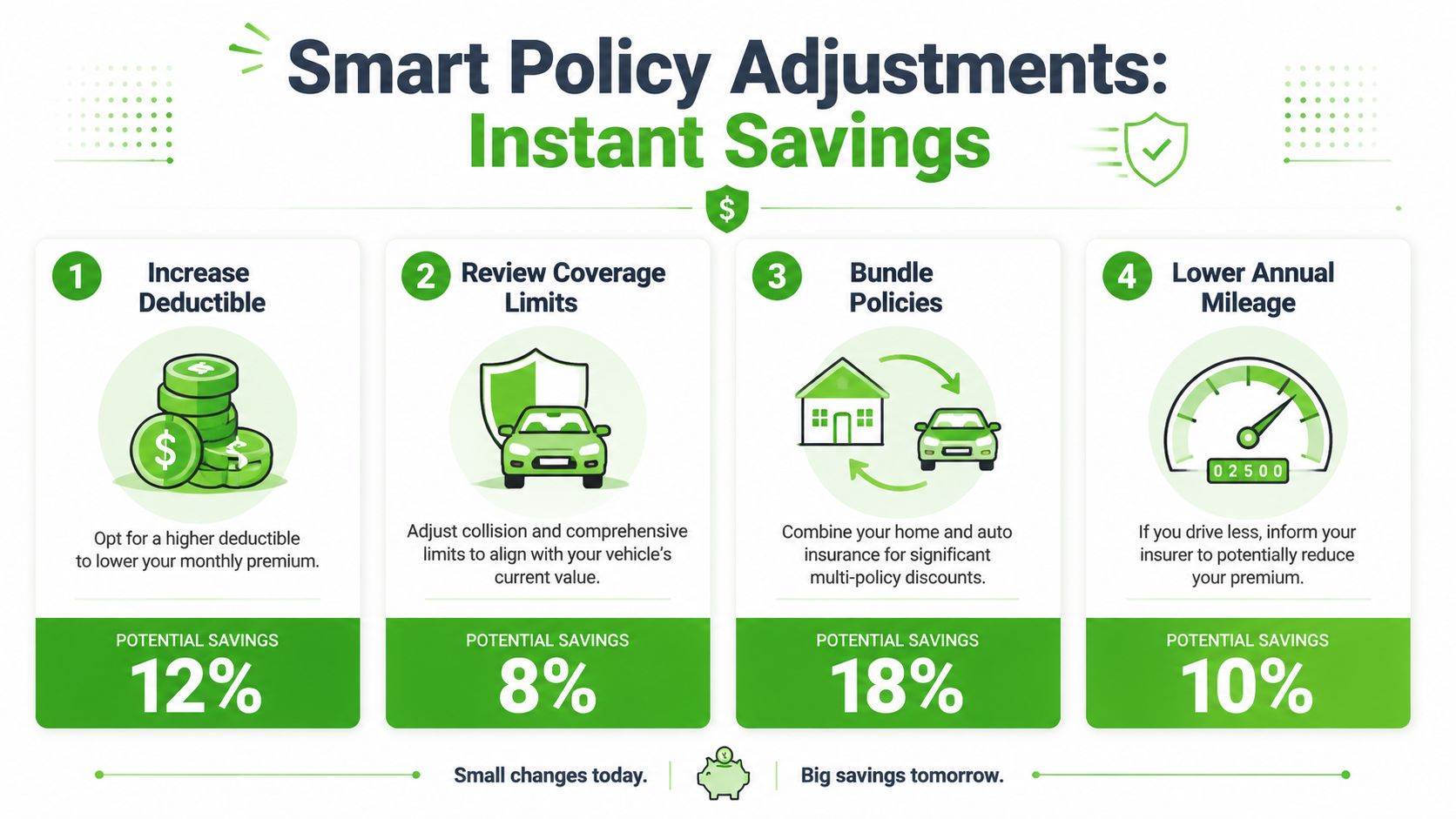

Raise the deductible only if your emergency cash can handle it

A higher deductible usually lowers the premium. That part is simple. The mistake is picking a deductible that looks good on paper and then scrambling for cash after a wreck, a cracked bumper, or hail damage.

Set the deductible at a number you can pay this week, not someday. If you cannot cover it from savings, it is too high. Georgia storms, heavy Atlanta traffic, and parking lot hits happen fast. A bad deductible choice turns a minor claim into a budget problem.

Use this rule: If you cannot pay the deductible without using a credit card, lower it.

Cut coverage that no longer makes sense for the car

Older cars get overinsured all the time. If your vehicle is worth little, paying for collision and additional vehicle protection may stop making financial sense, especially if the deductible eats up a big chunk of any payout.

Do the math. Check the car's current value, compare it to your annual premium for physical damage coverage, and ask what the insurer would pay after the deductible. If the answer is disappointing, trim the coverage and keep the savings.

This matters even more for Georgia drivers with a rough record. If a ticket or suspension already pushed the rate up, carrying extra coverage on a low-value car can make an expensive policy even worse.

Ask sharper questions when you call

Weak questions get weak answers. Call your insurer and make them rerate the policy using your current facts, not old assumptions from two renewals ago.

Ask these questions:

- What is the premium at each deductible option?

- Does collision still make sense based on this car's current value?

- Is my annual mileage rated correctly?

- Is there a cheaper payment option if I pay in full?

- Can you note any state-approved driver improvement course on my file?

That last one matters in Georgia. If you have points, a recent citation, or you are trying to show an insurer you are getting back on track, a Georgia defensive driving course discount with Progressive is the kind of practical step worth asking about during a policy review.

If you want another plain-English rundown of practical tips to save on coverage, read that before you make changes so you know which cuts save money and which cuts backfire.

Quick policy check table

| Policy issue | What to ask | Why it matters |

|---|---|---|

| Deductible set too low | Can you quote higher deductible options? | You may lower the premium if you can handle more out-of-pocket cost |

| Older vehicle | Does collision still make sense on this car? | You may be paying for coverage with limited real payout value |

| Payment method | Is paid-in-full cheaper than monthly billing? | Installments can cost more |

| Mileage estimate | Is my annual usage rated correctly? | Outdated mileage can keep the premium higher than it should be |

Unlock Every Possible Insurance Discount

A lot of drivers miss discounts because they assume the insurer applied everything automatically. Bad assumption. Carriers don't always volunteer the full list, and agents won't always know what matters in your situation unless you ask.

Ask for a discount audit, not a generic quote

Use that phrase. “I want a full discount audit on my policy.” Then make them go line by line.

Here's the checklist I'd use with any Georgia driver:

- Bundling with renters, homeowners, or another policy in the household

- Low-mileage status if you drive less than the carrier currently assumes

- Good student eligibility for younger drivers on the policy

- Occupation-based discounts that may apply to teachers, first responders, military, or other groups

- Vehicle safety equipment and anti-theft features

- Paperless or automatic payment options

- Safe-driver status if your record has improved

- Course completion discounts tied to documented driver improvement

Some of those won't apply. That's fine. The point is to force a real review instead of accepting the default rate.

Georgia drivers should ask about course-based savings

A lot of money gets left on the table. Insurers often recognize documented risk-reduction efforts better than vague promises that you'll “be more careful.”

If you want a Georgia-specific example of how carriers may handle this, look at the breakdown on the defensive driving course discount with Progressive. Even when a discount isn't automatic, having a state-approved course certificate gives you something concrete to submit and discuss.

Ask your insurer one direct question: “What proof do you accept for a driver-improvement or defensive-driving discount in Georgia?”

Don't wait for renewal to ask

Drivers in places like Gwinnett, DeKalb, and Cobb often wait until the renewal notice shows up. That's too late for some corrections. If your mileage dropped, if your teen driver moved off the policy, or if you completed a course, report it as soon as you can.

Discounts are rarely about luck. They usually go to the person willing to document, ask, and follow up.

Prove You Are a Safe Driver with Telematics

Telematics can save you money, but only if you understand what you're giving up in return. That's the honest answer.

These programs track how you drive through an app, a plug-in device, or built-in vehicle data. The insurer may look at braking, acceleration, time of day, mileage, and general driving patterns. If your habits look low-risk, you may get a better rate. If they don't, you may regret signing up.

AARP notes that telematics or usage-based insurance can lower premiums by about 10% to 15% on average, while also warning drivers to ask what data is collected and whether it can affect renewal pricing in its discussion of cutting car insurance premiums.

When telematics makes sense

Telematics fits drivers who already have disciplined habits:

- Shorter commutes and predictable mileage

- Smooth braking and acceleration

- Less late-night driving

- Confidence with app-based monitoring

If that sounds like you, the discount can be worth testing.

When I'd be cautious

If you do a lot of Atlanta stop-and-go driving, make frequent last-minute trips, or hand the car to a young driver who brakes hard and drives distracted, think twice. Telematics doesn't care about your intentions. It cares about recorded behavior.

You should also understand the privacy side before you enroll. Georgia drivers who want to improve habits first should start with the basics in these distracted driving prevention tips. Clean up the behavior, then decide whether you want it measured.

Before you sign up, ask what data is collected, how long it's stored, and whether poor driving data can hurt you later.

That last question matters. A small discount isn't always worth ongoing uncertainty if the carrier won't give a straight answer.

Lower Premiums with a Georgia Defensive Driving Course

Your rate jumps after a ticket. Then renewal hits, and the bill climbs again. In Georgia, a state-approved defensive driving course is one of the few steps that can help on both fronts. It can support an insurance discount and help you clean up the record that caused the problem.

Why insurers pay attention to the course

Insurance companies care about risk, not excuses. A completed defensive driving course gives you proof that you took a concrete step to drive better. Industry guidance regularly includes defensive driving classes among the standard ways drivers may cut premiums, and in Georgia, that advice has more value because the course can also help on the license side.

That matters most for drivers with blemishes on the record. If you already have points or a recent citation, you need something you can document. A certificate of completion gives you that.

Why it matters in Georgia

Georgia drivers get more practical value from this than drivers in many other states. A DDS-approved course can support an insurance discount with some carriers, and it may also reduce points from your driving record if you qualify. That is a real advantage when you are trying to stop one mistake from turning into years of higher premiums.

Here is the smart way to use the course:

- Take a DDS-approved class, not a random traffic course with no Georgia value

- Send the completion certificate to your insurer and ask for every discount tied to defensive driving

- Use it as part of a record-repair plan if tickets are already pushing your premium up

- Check whether you qualify to reduce points through this guide on removing points from your Georgia driving record

A lower bill matters. Keeping your record from getting worse matters more.

What a good class should actually teach

A useful course does more than help you check a box for the insurer. It should sharpen the habits that keep Georgia drivers out of trouble on I-75, I-285, and local roads where following too close, poor lane changes, distracted driving, and speed mistakes lead to citations fast.

Look for training that covers hazard recognition, space management, speed control, intersections, and impaired or distracted driver awareness in plain language. If you want a practical comparison point, these Skillz2Drive defensive driving insights show the kind of material that improves decision-making behind the wheel.

The course saves the most money when it helps you avoid the next ticket, not just explain the last one.

For Georgia drivers who need a DDS-approved option, Georgia DUI Schools offers defensive driving in online, live virtual, and classroom formats. That gives you realistic ways to get it done without rearranging your whole week.

Who should take one now

| Driver type | Why the course makes sense |

|---|---|

| Clean record driver | Gives you documented proof to request a discount and keeps sloppy habits from getting expensive |

| Driver with recent points | Helps you work on the behavior that causes repeat citations and may support point reduction if eligible |

| Older driver comparing quotes | Gives carriers one more reason to view you as lower risk |

| Driver coming off a suspension issue | Shows you are taking corrective steps instead of waiting for rates to fix themselves |

If you want a practical move that can save money now and reduce future damage, take the course. For a lot of Georgia drivers, it is one of the few steps that improves both the insurance file and the driving record.

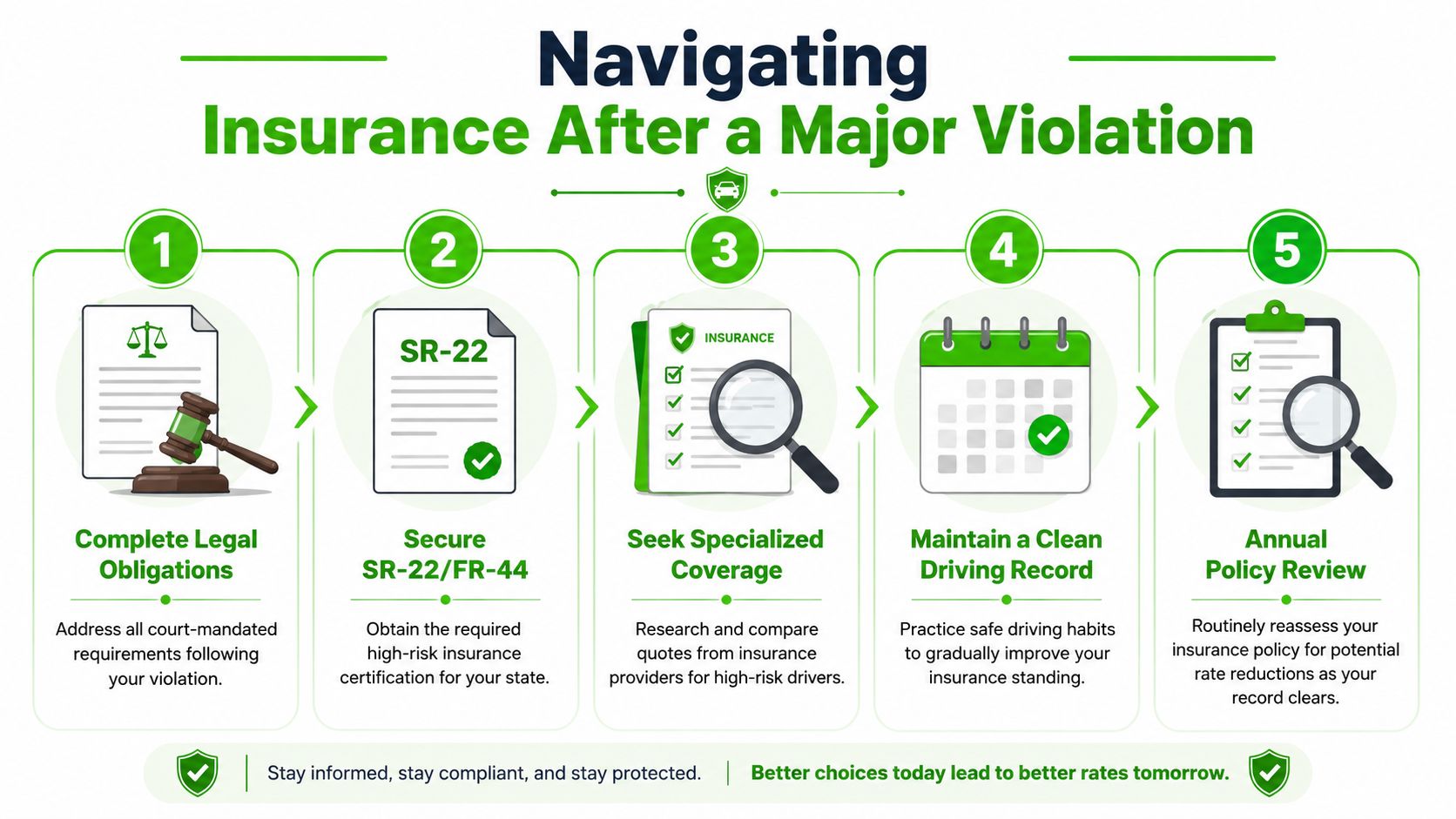

Regain Control After a DUI or Major Violation

After a DUI, serious ticket, suspension, or habitual offender issue, your insurance problem won't be solved by coupon-style discounts. You need a recovery plan.

The first priority is compliance. Finish what the court, DDS, or probation process requires. In Georgia, that can include a DUI Risk Reduction course, a clinical evaluation, treatment recommendations, and other reinstatement steps depending on the case. None of that is optional if you want your license back and your insurance situation to improve over time.

What to focus on first

- Complete every required program and keep your paperwork organized.

- Fix the license side before the shopping side because insurers price uncertainty badly.

- Shop carriers that write higher-risk drivers instead of wasting time with companies that clearly don't want the case.

- Keep the next year boring. No missed court obligations. No new tickets. No sloppy driving.

If your record already has points attached, start with this guide on how to remove points from your driving record. It won't erase a DUI, but it can help you stop additional record damage from stacking up.

The hard truth after a major violation

You probably won't get the rate you want right away. That's normal. The win at this stage is different. The win is becoming insurable at a more reasonable price over time by showing compliance, stability, and safer behavior.

Drivers in Georgia get through this every day. The ones who recover fastest are the ones who stop looking for shortcuts and start building a cleaner file.

If you need the next practical step, enroll in a course that matches your situation. For drivers focused on lowering premiums and improving a record, start with the Georgia Defensive Driving Course.