You open your renewal notice, scan down to the premium, and pause. You’ve driven Georgia roads for decades. You don’t race down I-285, you don’t drive much at night, and you may even have a spotless record. Yet the price still climbed.

That’s one of the most frustrating parts of shopping for the best car insurance for older drivers. Experience helps, but age can still change how insurers price risk. For many Georgia seniors, the answer isn’t just “switch companies.” It’s understanding why the rate changed, which discounts matter, and when a state-approved course can help you lower costs or repair a record after a violation.

Georgia drivers also face local issues that national articles usually skip. A retiree in Athens who only drives to church, the grocery store, and doctor visits needs a different strategy than an Atlanta driver trying to reinstate a license after a DUI. If you want a quick sense of the broader market before comparing policies, this overview of car insurance rates in Georgia is a useful starting point.

Your Guide to Navigating Senior Car Insurance in Georgia

If you’re an older driver in Georgia, insurance shopping gets easier when you separate the problem into three parts.

First, figure out why your premium changed. Many drivers assume a rate increase means the company thinks they’ve become reckless. That usually isn’t the issue. Insurers often look at injury risk, claim cost, mileage patterns, and recent violations differently once a driver reaches later life stages.

Second, decide what kind of driver you are right now, not what kind you were ten years ago. A clean-record retiree who drives short daytime trips should shop differently from someone who recently got a ticket, needs a defensive driving certificate, or must complete the Georgia Risk Reduction process after a DUI.

Third, compare insurance options with Georgia rules in mind. That includes:

- Discount planning: Ask about mature driver savings, low-mileage programs, bundling, and safe-driver rewards.

- Course strategy: A state-approved defensive driving course can help with point reduction and may also help with premium savings.

- High-risk recovery: If you’ve had a DUI or major violation, the path back usually starts with required education and license reinstatement steps before you can seriously compare quotes.

Practical rule: Don’t treat your insurance renewal like a final bill. Treat it like an opening offer.

That mindset matters. A senior driver in Marietta with a clean record may focus on mileage and safe-driver discounts. A driver in Macon dealing with a suspension or reinstatement issue may need to complete required courses first, then shop carriers that still write high-risk policies.

Why Car Insurance Costs Change for Experienced Georgia Drivers

Many older drivers ask the same question: “If I’m driving less and driving more carefully, why is my rate going up?”

The short answer is that insurers don’t look only at how often crashes happen. They also look at how expensive a crash becomes when it does happen. According to The Zebra’s senior driver insurance analysis, drivers age 60 and older see a 32% increase in average car insurance premiums as they age, rising from $1,934 annually at age 60 to $2,089 by age 70. That same analysis explains that the increase is tied largely to claim severity, because older drivers are more likely to suffer serious injuries in a crash.

Frequency and severity are not the same thing

This distinction confuses people because it feels unfair at first.

Think of insurance like roofing. Two homes may each have one storm claim. But if one home has minor shingle damage and the other has major structural damage, the second claim costs far more. Insurers apply similar thinking to auto coverage. They may view an older driver as careful overall, while still expecting a higher medical payout if a collision happens.

That’s why a long driving history doesn’t always keep rates flat in later years.

What insurers are really pricing

Insurers usually price several moving parts at once:

- Injury exposure: Older adults can be more physically vulnerable in a crash, even a moderate one.

- Recovery cost: Medical treatment and follow-up care may be more expensive when injuries are more serious.

- Driving changes: Vision, hearing, flexibility, and reaction time can shift gradually, even for drivers who remain responsible and alert.

- Vehicle use patterns: Some retirees drive less, but some also make more short trips in local traffic, parking lots, and busy daytime conditions.

None of this means an older driver is automatically unsafe. It means the insurance company is pricing the possible size of a future claim, not just the odds of a fender bender.

A safe driving history still matters. It just isn’t the only factor on the worksheet.

Georgia drivers should think locally

Georgia adds another layer. Metro Atlanta traffic, suburban lane changes, rural night driving, and heavy medical claim costs all affect how a carrier sees risk. A driver in Roswell who rarely commutes may still face a higher renewal because the insurer’s model gives more weight to injury severity than to years of accident-free driving.

That’s why the best response isn’t anger. It’s strategy.

Once you understand the insurer’s logic, the next move becomes clearer. Look for companies that reward mature drivers in specific ways, and look for discounts tied to low mileage, clean driving, and approved courses.

Key Discounts and Top Insurers for Older Georgians

Not every discount matters equally for senior drivers. Some sound helpful but barely move the needle. Others can make a real difference if they match your driving habits.

The strongest starting point is to ask each insurer how they handle mature drivers who don’t commute much, keep a clean record, and can document safe-driving education. According to InsuredBetter’s review of senior auto insurance options, top insurers for seniors include The Hartford’s AARP program for drivers 50+, USAA for veterans, and Nationwide for low-mileage programs.

Discounts older Georgia drivers should ask about

Some discounts are obvious. Some are easy to miss unless you ask directly.

- Mature driver discounts: These are designed for older, experienced motorists and may pair well with a clean record.

- Low-mileage savings: Retirees often qualify because they drive fewer miles than working commuters.

- Bundling: If you carry homeowners, renters, or another policy with the same company, bundling may lower total cost.

- Accident-free rewards: If you’ve gone years without a claim, ask whether the company applies a safe-driver credit automatically or only on request.

- Telematics or usage-based programs: These can help if you avoid hard braking, speeding, and nighttime driving.

- Veteran or military eligibility: This matters for households that qualify for USAA.

- Course-based discounts: A defensive driving certificate may support savings and can be especially useful if you’re also managing points.

What makes a senior-focused insurer useful

The best car insurance for older drivers isn’t always the one with the lowest advertised price. It’s the one that fits your life.

A widow in Savannah who drives short trips might value simple billing, roadside help, and low-mileage options. A retired veteran in Columbus might find a better fit with a carrier that understands military households. An AARP member in Alpharetta may care most about mature-driver benefits and phone support that’s easy to reach.

Here’s a practical comparison framework.

Top Car Insurance Providers for Georgia Seniors in 2026

| Insurer | Best For | Key Senior Discounts |

|---|---|---|

| The Hartford AARP Program | Drivers 50+ seeking senior-focused coverage | Mature driver and other senior-oriented discounts |

| USAA | Veterans and military families | Military-focused value and senior-friendly pricing approach |

| Nationwide | Retirees and other low-mileage drivers | Low-mileage programs |

| State Farm | Drivers asking about mature driver discounts | Mature-driver oriented discount options |

If you want a broader action plan beyond just carrier names, this guide on how to lower car insurance rates is useful for organizing what to ask before you request quotes.

How to use the table without getting misled

Don’t call one company and stop there. Use the table as a shortlist, not a conclusion.

When you contact each insurer, ask these questions in plain language:

- “Do you offer a discount for mature drivers or drivers over a certain age?”

- “How do you rate low annual mileage for retirees?”

- “Will a Georgia defensive driving certificate affect my premium?”

- “Do you have a telematics option, and is it a good fit for someone who mostly drives daytime local trips?”

- “If I bundle home and auto, what changes?”

Smart comparison habit: Ask every company for the same coverage limits and deductibles. Otherwise, one quote may only look cheaper because it covers less.

That last point matters a lot. One policy may include stronger liability protection, roadside assistance, or better claim support. Another may look cheaper until you notice a much higher deductible. Compare like with like.

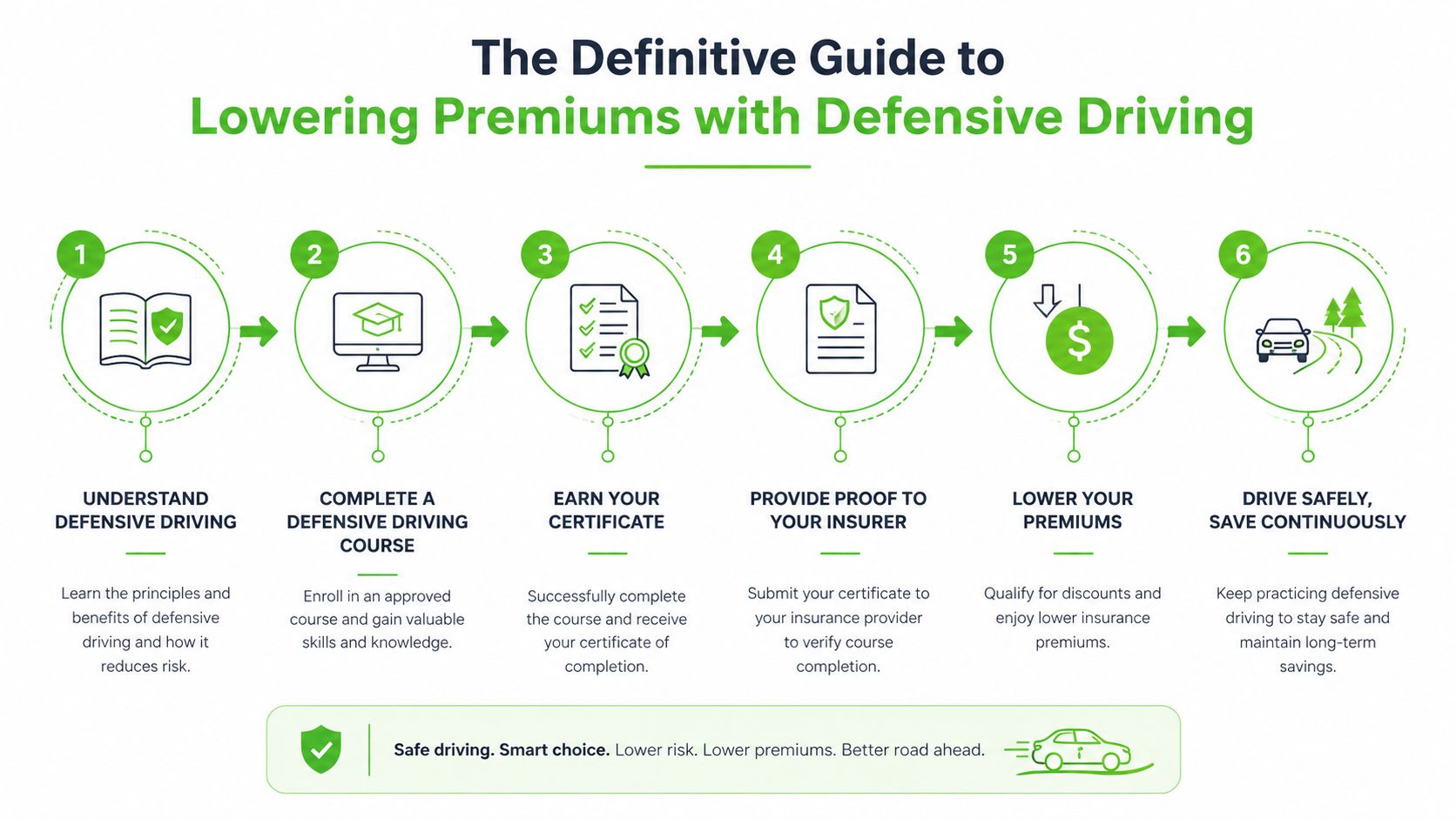

The Definitive Guide to Lowering Premiums with Defensive Driving

If there’s one step many older Georgia drivers overlook, it’s defensive driving.

People sometimes hear that phrase and think it’s only for teenagers, court cases, or people who drive aggressively. That’s not true. For seniors, a defensive driving course is often a practical money tool and a safety refresher at the same time.

According to The Zebra’s review of good-driver discounts, GEICO’s Accident-Free Good Driver discount can reach 26%, and that can stack with senior-specific perks. The same source notes that enrolling in a defensive driving course can further slash premiums by 10% to 20%, and that the hazard-perception skills reinforced in elder retraining have been shown to cut crash rates by 12% to 18%.

Why defensive driving matters more for older drivers

A good course doesn’t just repeat obvious rules. It refreshes habits that directly affect claims and violations:

- Scanning intersections earlier

- Managing following distance

- Handling left turns in heavy traffic

- Adjusting for glare, rain, and nighttime limits

- Recognizing when medication, fatigue, or stress affect alertness

That’s why insurers and Georgia drivers both care about it. The course helps you become easier to insure because it supports the exact driving behaviors companies want to reward.

How the Georgia process helps

In Georgia, a state-approved defensive driving course can serve two practical purposes.

First, it may help you qualify for an insurance discount, depending on the carrier and your policy. Second, it can help with point reduction in the right situation. For an older driver with a minor ticket, that can matter a lot. Fewer points can mean a cleaner record presentation when you shop quotes.

The process is usually straightforward:

- Choose a Georgia-approved course format.

- Complete the class and keep your certificate.

- Send proof to your insurer if they request it.

- Ask the agent to re-rate the policy with the course applied.

- If points are involved, confirm the DDS handling and timing.

For drivers who want a format built around mature-driver concerns, this defensive driving course for seniors gives a Georgia-specific option.

Online, classroom, or live virtual

This part trips people up. They assume one format is “official” and the others are not. What matters is state approval, not whether you sat in a classroom chair.

Different drivers do better with different settings:

- Online self-paced learning: Good if you want breaks, larger screens, and time to review.

- Live virtual instruction: Useful if you learn better with a real instructor and questions.

- In-person classroom: Some drivers prefer face-to-face structure and fewer technology hurdles.

Georgia DUI Schools offers defensive driving in online, live virtual, and classroom formats, which can be practical for drivers in Atlanta, Athens, and other Georgia communities who need flexibility.

Some seniors save the most money not by switching insurers first, but by making themselves easier to underwrite before they shop.

How to talk to your insurer after completion

Don’t just finish the class and file the certificate away.

Call your insurer and ask direct questions:

- “Do you apply a discount for this Georgia-approved course?”

- “How long does the discount stay on the policy?”

- “Do I need to email or upload the certificate?”

- “Will this also help if I’m comparing a rewritten policy or a renewal?”

Write down the representative’s name and what they told you. If you’re shopping several carriers, mention the completed course in every quote request. The value of the course often shows up more clearly when multiple companies re-rate your policy.

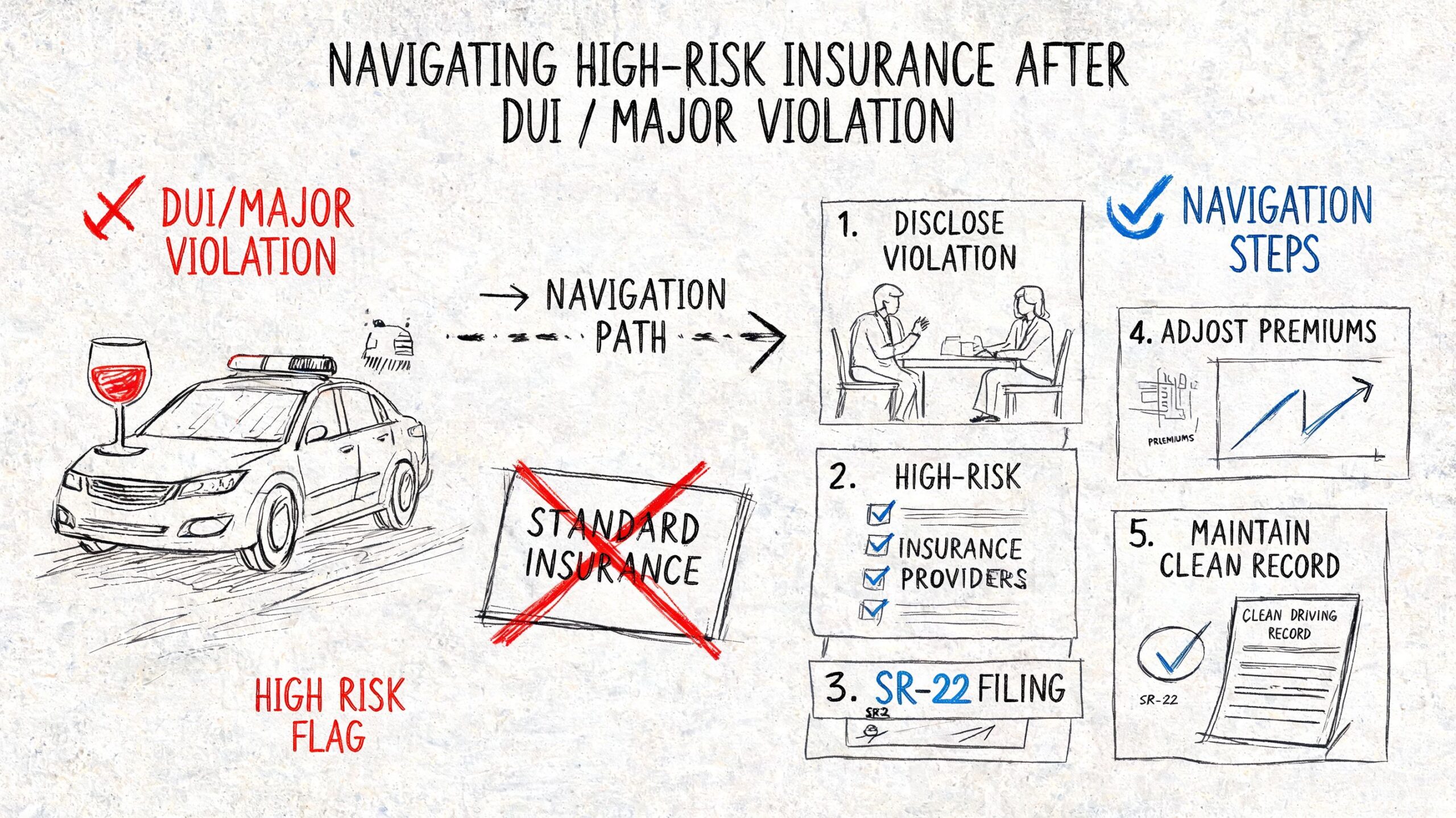

Navigating High-Risk Insurance After a DUI or Major Violation

A DUI changes the conversation fast. For an older driver, it can feel especially discouraging because one incident can wipe out years of safe-driving credibility.

Still, there is a path forward in Georgia. It starts with accepting two facts. First, some insurers may refuse to write the policy at all. Second, the companies that will insure you usually want to see that you’ve completed every required state step.

According to LendingTree’s discussion of senior insurance and high-risk situations, many insurers deny coverage after a DUI, while State Farm and American Family are often recommended for high-risk drivers, potentially saving over $600 per year compared with standard high-risk surcharges.

What Georgia drivers usually need first

If you’re dealing with a DUI-related suspension or reinstatement issue, insurance shopping is only part of the job.

Georgia drivers often need to address:

- Risk Reduction course completion: Commonly called DUI School, this is often tied to reinstatement requirements.

- Clinical evaluation: Some drivers must complete an evaluation before moving further in the process.

- Additional treatment or follow-up requirements: Depending on the case, that may include ASAM-related recommendations or other steps.

- Proof and paperwork: Keep every completion document organized before you contact insurers.

A high-risk insurer may still quote you, but your position improves when you can show that you’ve completed what Georgia requires.

How older drivers should approach the market after a DUI

Don’t shop this situation the same way a clean-record driver would.

Instead, do this:

- Finish required state steps first. If reinstatement work is incomplete, insurance shopping may be premature.

- Ask carriers whether they still write DUI-related policies. Save time by screening for appetite early.

- Use your completed coursework as part of your story. It won’t erase the violation, but it shows compliance and effort.

- Request identical quote structures. High-risk quotes are hard enough to compare without changing deductibles and limits.

- Prepare for follow-up underwriting questions. Carriers may ask about timing, violations, and license status.

If you’re trying to understand how long the violation continues to affect your insurance search, this guide on how long a DUI stays on record in Georgia can help you frame the timeline.

A DUI creates a pricing problem, but it also creates a paperwork problem. Solving both matters.

Don’t ignore the education side

Many older drivers focus only on the insurance card and forget the larger reinstatement picture. That’s risky. A carrier may issue a policy, but if your state requirements are incomplete, you still haven’t solved the core problem.

For seniors, this can be emotionally heavy because driving often means independence. That’s exactly why a structured plan matters. Complete the required course work, follow through on evaluations if ordered, gather proof, then approach insurers that are known to consider high-risk drivers.

A Step-by-Step Checklist for Shopping and Comparing Quotes

Shopping for the best car insurance for older drivers gets easier when you stop doing it from memory. Build a small file first, then compare quotes on equal terms.

A useful benchmark comes from NerdWallet’s senior auto insurance review, which notes that Mapfre can offer full coverage for as low as $101 per month for a 70-year-old driver with a clean record. That doesn’t mean you’ll get the same price, but it gives you a target when you start asking for quotes after every eligible discount is applied.

Your quote-shopping checklist

Gather the basics

Have your driver’s license, vehicle information, current declarations page, and estimated annual mileage ready. If you recently completed a defensive driving course, keep that certificate nearby too.List every driver and every issue

Include everyone on the policy and note tickets, accidents, or a DUI if applicable. It’s better to be accurate up front than to get a quote that changes later.Choose one coverage structure

Pick the same liability limits, deductibles, and add-ons for every quote request. If one quote includes roadside assistance and another doesn’t, you’re not making a true comparison.Ask about senior-relevant discounts

Mention mature-driver status, low mileage, accident-free history, telematics, bundling, and course completion.Get multiple quotes close together

Rates can shift, and timing matters. Gathering quotes in a short window gives you a cleaner comparison.

Questions that uncover hidden savings

Use simple language when speaking with an agent.

- “Am I being rated as a low-mileage driver?”

- “Did you include any mature-driver or safe-driver discount?”

- “Would this price change if I bundle another policy?”

- “Does a completed Georgia defensive driving course change the premium?”

- “Is this quote based on the same deductibles as my current policy?”

Some drivers prefer to work with a local independent agency so they can compare several companies without repeating the same conversation over and over. If that sounds helpful, a place to compare affordable insurance can simplify the quote-gathering process.

How to read the final numbers

Don’t stop at the premium.

Look at:

- Liability limits

- Deductible size

- Whether the car’s value still justifies full coverage

- Claims service reputation

- Whether the insurer handles high-risk histories or only clean records well

A lower premium can be a smart move. It can also be a trap if the policy is stripped down too far.

Frequently Asked Questions for Senior Drivers in Georgia

Will my rates automatically go down after a defensive driving course

Usually, no. You often need to ask for the discount and provide proof of completion. Some insurers apply eligible discounts more smoothly than others, but it’s wise to call and confirm that the course has been added to your policy.

Is a car with modern safety features cheaper to insure

Sometimes, yes, but not always in a simple way. Safety features can help an insurer view the vehicle more favorably, but repair costs, parts prices, and claim patterns also matter. Ask for quotes on the exact vehicle before you buy or replace a car.

If you’re changing vehicles in retirement, compare insurance costs before signing the purchase papers.

Should I keep full coverage on an older car

That depends on the car’s value, your savings, and how much risk you can comfortably absorb. If the vehicle is worth relatively little, paying for collision and coverage for other types of damage may stop making financial sense. On the other hand, if replacing the car out of pocket would be difficult, keeping broader coverage may still be the safer choice.

What if I had a DUI years ago and need insurance now

You may still find coverage, but you’ll want to shop carefully and be ready to explain your current status. If Georgia required coursework, evaluation, or reinstatement steps in your case, complete those first and keep your paperwork organized. That won’t erase the past, but it puts you in a better position.

Do I need to tell the DDS about a medical condition

That depends on the condition and the situation. If a medical issue affects safe driving, it can have licensing consequences as well as insurance consequences. When in doubt, get guidance early and keep records of any evaluations or restrictions.

Is telematics a good idea for older drivers

It can be. If you drive short daytime trips, avoid hard braking, and rarely speed, a telematics program may help. If you dislike tracking technology or your driving pattern includes frequent stop-and-go traffic that could work against you, ask how the program is scored before enrolling.

What’s the single best next step if I want lower premiums

For many older Georgia drivers, it’s completing a state-approved defensive driving course and then shopping quotes with that certificate in hand. That step can help clean-record drivers, and it can also support a broader recovery plan after a violation.

If you’re ready to take a practical next step, Georgia drivers can start with Georgia DUI Schools and review the course option that fits their situation, especially a defensive driving course for lowering premiums or a Risk Reduction course if reinstatement is part of the process.