If you’re trying to lower your car insurance, you really have three main levers to pull: keeping your driving record clean, hunting down every possible discount, and tweaking your coverage and deductibles. But if you want the fastest, most surefire way to get a discount, completing a state-approved defensive driving course is your best bet.

Why Georgia Car Insurance Rates Are So High

Noticed your car insurance bill creeping up, even with a spotless driving record? You’re not imagining things. A lot of Georgia drivers are asking the same question, and the answer is a mix of statewide issues and national trends that hit everyone’s wallet.

Getting a handle on these bigger-picture factors is the first step to becoming a savvier insurance shopper. It’s not always about your driving; sometimes, it’s about the economic climate insurance companies are operating in.

The Rising Cost of Everything

One of the biggest culprits behind higher premiums is the shocking cost of vehicle repairs today. Modern cars are loaded with high-tech features like sensors, cameras, and advanced driver-assistance systems (ADAS). While they make us safer, they are incredibly expensive to fix or replace after an accident.

What used to be a simple fender bender costing a few hundred bucks can now easily turn into a multi-thousand-dollar repair just to recalibrate the sensors in your bumper. Those skyrocketing repair costs get passed straight to us through higher insurance premiums for everyone.

On top of that, medical costs just keep climbing. Since your liability coverage pays for injuries to other people when you’re at fault, the rising price of healthcare has a direct line to insurance payouts and, you guessed it, your rates.

Georgia’s Unique Challenges

Beyond the national issues, a few things specific to the Peach State help give us some of the highest insurance costs in the nation.

- Heavy Traffic: Major hubs, especially Atlanta, are notorious for gridlock. The “Spaghetti Junction” on I-85 and I-285 isn’t just a local landmark; it’s a hotbed for accidents. More cars crammed onto the road simply means more chances for accidents to happen.

- More Serious Accidents: Sadly, factors like higher speeds and distracted driving are leading to more severe—and more expensive—crashes across the state.

- Wild Weather: Georgia gets hit with everything from tornadoes in the north Georgia mountains and hailstorms in the suburbs to hurricanes along the coast near Savannah. These events trigger a ton of comprehensive claims, which drives up rates for all of us.

- Too Many Uninsured Drivers: When someone without insurance hits you, your own policy has to cover the damage. States with more uninsured drivers, like Georgia, often have higher base rates to offset that risk.

The hard truth is that your insurance rate is a reflection of shared risk. Even if you’re a perfect driver in a quiet town like Dahlonega, your premium is still affected by the sheer number of claims filed in traffic-choked zones like I-285 in Atlanta.

A Glimmer of Hope on the Horizon

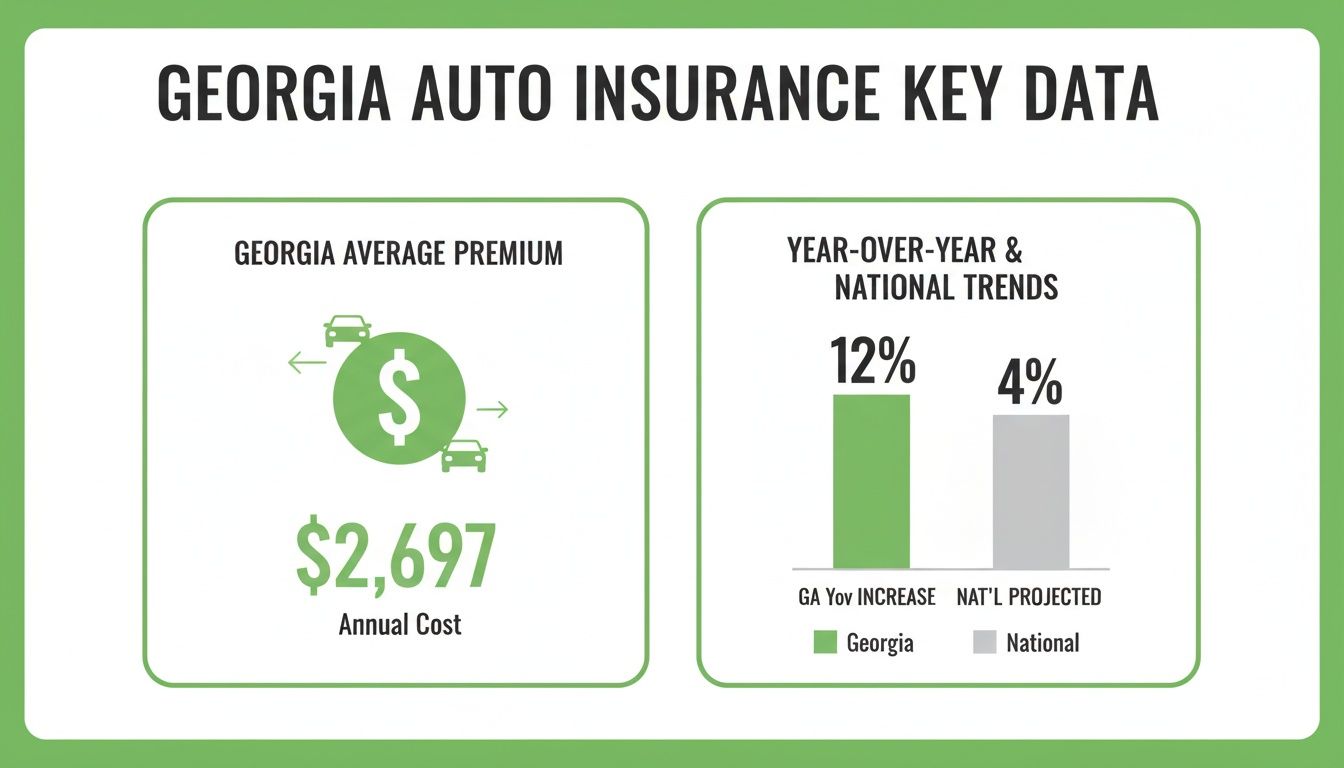

While all that sounds pretty grim, there are signs that the worst of the price hikes might be slowing down. As of March 2026, the average annual premium for full coverage sits at $2,697, which works out to about $225 per month. Yes, that’s a 12% increase since 2024, but it’s a much slower climb than we’ve seen in previous years.

In fact, industry experts are forecasting a more reasonable national increase of around 4% for 2026, suggesting the market is finally starting to level off. You can find more details about national auto insurance cost trends on Bankrate.com.

This stabilization means now is the perfect time to get proactive. By understanding why your bill is so high, you can use the strategies we’re about to cover to fight back and make sure you’re not paying a dime more than you have to.

Your Driving Record Is Your Biggest Money-Saver (or Expense)

When it comes to your car insurance bill, nothing matters more than your driving record. To an insurance company, a driver with a history of tickets and accidents is a financial risk. A clean record, on the other hand, tells them you’re a safe bet, and they’ll reward you with a lower premium.

Every single time you get behind the wheel, you’re making a choice that either protects your good rate or gives your insurer a reason to jack it up. A single at-fault fender-bender can wipe out years of “good driver” status, costing you a fortune over time.

And in Georgia, the stakes are higher than ever.

While rates are rising everywhere, Georgia’s costs are climbing three times faster than the national average. That makes keeping a clean driving record one of your best defenses against a shockingly high bill.

How a Single Ticket Can Wreck Your Rate

Insurance companies don’t look at all violations the same way. A parking ticket isn’t a big deal, but a speeding ticket or reckless driving charge is a major red flag. These incidents don’t just go away; they stay on your driving record for years, inflating your rates until they finally expire.

Just look at how different violations can send your premium soaring:

- Speeding Tickets: Even one ticket can hike your rate by 15-25%. Get a couple of them, and insurers see a pattern of risky behavior, leading to even bigger increases.

- At-Fault Accidents: If you cause an accident, expect a serious financial hit. Your premium could easily jump 30-50% or more, depending on how bad the damage was.

- Reckless Driving: This is a huge one. A reckless driving conviction can nearly double what you pay for insurance. It paints you as a high-risk driver, making it tough to find affordable coverage from anyone.

These aren’t just one-time fines. They are penalties you pay over and over again for years. Some driving is so out of line it grabs headlines, like the driver clocked going 109mph on I-285 on New Year’s Eve. The insurance consequences for that are astronomical.

To see how this plays out in real numbers, take a look at the average increases drivers face.

How Driving Incidents Affect Your Georgia Insurance Premium

| Driving Violation | Average Premium Increase (Percentage) | Typical Duration on Record (Years) |

|---|---|---|

| Speeding (16-29 mph over) | 24% | 3-5 |

| At-Fault Accident | 49% | 3-5 |

| Reckless Driving | 98% | 3-5 |

| DUI (First Offense) | 85% | 5-10 |

These figures show just how much a single mistake can cost you. The violation stays on your record for years, meaning you’ll be paying that higher premium again and again until it finally drops off.

What the Georgia Points System Means for You

The Georgia Department of Driver Services (DDS) tracks your violations using a points system. If you rack up 15 or more points in a 24-month period, your license gets suspended.

While your insurance company cares more about the violation itself (like speeding or an accident), those points create an official “risk score” that they absolutely pay attention to. More points signal more risk, which justifies a higher premium.

For example, getting caught going 19-23 mph over the speed limit adds 3 points. A reckless driving charge adds 4 points, and aggressive driving tacks on 6 points. Insurers see this activity and know it’s time to re-evaluate your rate.

How to Clean Up Your Record and Lower Your Rate

If you’ve got a few marks on your record, don’t panic. You have options.

The most direct way to get back in control is by completing a state-approved defensive driving course. In Georgia, you can get up to 7 points removed from your license once every five years by taking a certified six-hour program.

This move gives you two huge wins. First, you lower your point total, which helps you steer clear of a license suspension. Second, you send a clear message to your insurance company that you’re serious about being a safer driver. Many insurers offer a discount of 5-15% for completing a course—an instant and effective way to cut your car insurance costs.

Find Every Car Insurance Discount You Qualify For

While a clean driving record pays off over time, hunting for discounts is the quickest way to lower your car insurance bill right now. The truth is, most drivers are eligible for at least a few discounts, but they’re leaving money on the table because they just don’t know what’s available.

Don’t expect your insurance company to hand you a list of every single discount you qualify for. You have to be your own advocate. Think of it as a quick treasure hunt where finding even one or two new discounts means real cash in your pocket every month.

Go Beyond the Obvious Discounts

Everyone knows about the good driver and bundling discounts. That’s the easy stuff. The real savings come from digging a little deeper into the less-common discounts that many Georgia insurers offer.

These hidden gems usually fall into a few key areas related to you, your car, and how you pay.

Driver-Based Discounts

- Good Student: Have a high school or college student on your policy holding down a “B” average or better? That can knock off up to 15%.

- Defensive Driving Course: As we’ll cover later, completing a state-approved course is a guaranteed way to get a discount.

- Affinity Groups: This is a big one people miss all the time. Are you a teacher in Fulton County? A nurse at Northside Hospital? A UGA grad? Many insurers offer discounts to members of certain professions, alumni associations, or even employees of large local companies like Delta or Coca-Cola.

Vehicle-Based Discounts

- Anti-Theft Devices: If your car came with a factory alarm, an engine immobilizer, or you have a tracking service like LoJack, you should be getting a discount.

- Newer Vehicle: Cars less than three years old often get a small rate cut because they’re seen as more reliable and packed with modern safety gear.

- Safety Features: Things like anti-lock brakes (ABS), airbags, and electronic stability control can each add a small, stackable discount to your policy.

Think of your policy as a puzzle, and each discount is a piece. The goal is to find every piece that fits. A 3% discount here and a 5% discount there can easily add up to hundreds of dollars in savings each year.

Policy and Payment Discounts

How you manage your policy can also chip away at your premium. Insurance companies love customers who are easy to work with and financially stable.

For instance, you can often get a nice discount for paying your entire six-month or annual premium upfront instead of month-to-month. It saves them billing hassles, and they’ll pass some of those savings back to you.

Two other easy wins are signing up for paperless billing and automatic payments (EFT). Each one might only save you $5 or $10 per policy period, but it costs you nothing and every little bit helps.

And don’t forget about loyalty. If you’ve stuck with the same company for several years with no claims, ask if they offer a loyalty discount. Just don’t let that loyalty blind you—it’s still smart to shop around every year to make sure their “loyal” price is actually competitive.

Your 30-Minute Discount-Finding Mission

Alright, it’s time to take action. Don’t wait for your renewal notice. Grab your policy number, set aside 30 minutes, and call your insurance agent with a specific list of questions.

- Start Broad: “Could you walk me through every single discount I’m currently getting on my policy?”

- Ask About Your Job & School: “Do you have any discounts for my job as a [teacher, nurse, etc.] or for alumni of [Your University]?” For instance, ask about a UGA alumni discount or one for working at a major Georgia employer.

- Confirm Vehicle Features: “I just want to confirm I’m getting all possible discounts for my car’s features, like its anti-lock brakes and factory alarm. Can you check that for me?”

- Mention Your Mileage: “I drive less than 7,500 miles a year. Do I qualify for a low-mileage discount?”

- Check Payment Options: “How much would I save by paying my premium in full? And what about for switching to auto-pay and paperless billing?”

Making that one phone call puts the power back in your hands. You’ll know exactly where you stand and how much you can save.

Use a Defensive Driving Course to Guarantee a Discount

Want one of the surest, quickest ways to get a discount on your car insurance? Take a defensive driving course. It’s a direct, proactive step that puts money right back into your wallet.

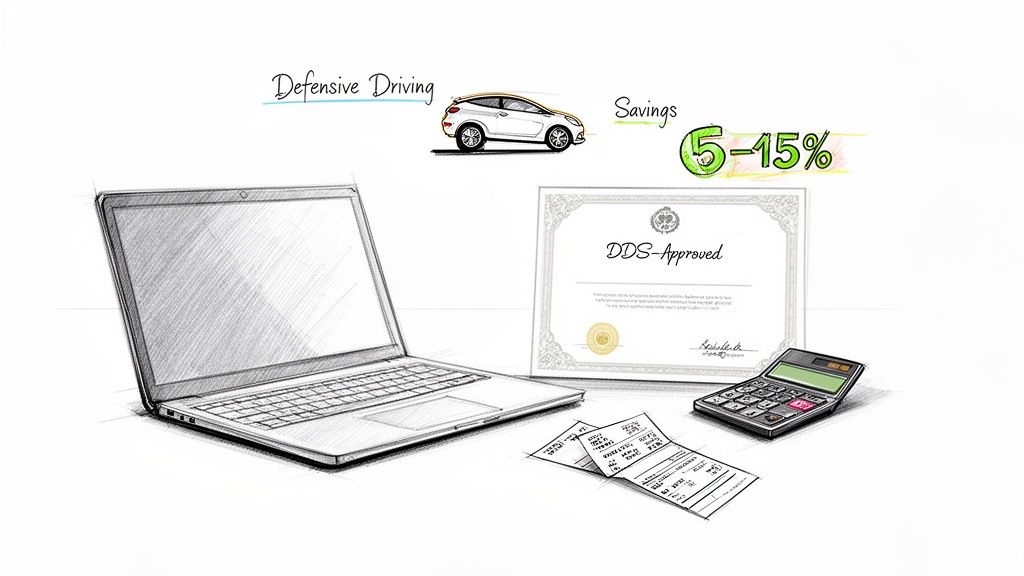

Here in Georgia, when you finish a state-certified defensive driving program, it proves to your insurer that you’re serious about safety. In return, almost every carrier is required to give you a premium discount, which usually sticks around for three years. It’s a simple deal: spend a few hours learning, get an immediate financial reward.

The Simple Math Behind the Savings

You might think a defensive driving course is just another expense, but a quick look at the numbers shows it’s a smart investment. The course often pays for itself within the first year alone.

Let’s get into it. Georgia insurance providers offer discounts ranging from 5% to 15% for drivers who complete a certified course. With the average full-coverage premium in Georgia sitting at $2,697 a year, that’s a potential savings of $135 to $405 annually.

Most approved courses cost around $95. You do the math.

Think of it this way: You spend about $95 on a six-hour course and, in return, you could save over $400 on your insurance bill. That’s a significant return for a small time commitment, making it one of the smartest financial moves a driver can make.

Since the discount is good for three years, your total savings could easily top $1,200. Not bad for a one-time class.

Finding a Course That Fits Your Life

Forget the old days of being stuck in a bland classroom all Saturday. Today, Georgia DDS-approved courses come in a few different flavors, so you can pick what works for you.

- Self-Paced Online: The ultimate in flexibility. Log on from home in Valdosta or during your lunch break in Atlanta. Work at your own speed, whenever you have time.

- Live Virtual (Zoom): Want a classroom feel without the commute? Zoom classes give you a live instructor to answer questions and keep you on track.

- Traditional Classroom: If you learn best with in-person instruction, you can still find classroom sessions in communities from Athens to Savannah.

More Than Just a Discount

The insurance discount is a great perk, but it’s not the only one. The skills you sharpen in a defensive driving course help you avoid accidents and tickets in the first place—which also keeps your rates from skyrocketing.

There’s more on the additional benefits of defensive driving in our detailed guide.

This one course can even pull double or triple duty. If you have a few points on your license, completing the program can knock off up to seven points, helping you steer clear of a suspension.

At the end of the day, a defensive driving course is an investment in yourself. It makes you a safer driver, keeps your record clean, and offers a guaranteed way to lower your car insurance bill. It’s a clear win.

Make Smart Policy Adjustments and Shop Around

Letting your car insurance policy sit on auto-renew is one of the biggest and most common mistakes you can make. While keeping a clean record is a great start, the real power moves for saving money come from actively managing your policy and shopping around. It’s time to get hands-on with your insurance.

Many drivers just assume their loyalty gets them the best deal. The hard truth? It rarely does. Insurance rates are always shifting, and last year’s bargain could be this year’s ripoff. You have to be your own best advocate.

Rethink Your Deductibles

One of the fastest ways to lower your monthly premium is to adjust your deductible. This is the amount you agree to pay out-of-pocket on a comprehensive or collision claim before your insurance company pays a dime.

Think of it as a trade-off. A higher deductible means you’re taking on more of the initial risk, and in return, your insurer gives you a lower premium. For example, if you’re driving a 10-year-old car that’s paid off, bumping your deductible from $500 to $1,000 is a smart move. It could save you a good chunk of change, and you might not even file a claim for minor damage on an older car anyway.

On the other hand, if you just drove a new car off the lot, a lower $500 deductible probably makes more sense to protect your investment. The key is finding that sweet spot: a deductible high enough to save you money, but low enough that you could comfortably write a check for it tomorrow if you had to.

Review Your Coverage Limits

Your coverage limits are another place to find savings, especially with older vehicles. If your car isn’t worth much anymore, paying for full comprehensive and collision coverage might just be a waste of money.

Here’s a good rule of thumb I always tell people: if your annual premium for comprehensive and collision is more than 10% of your car’s Blue Book value, it’s probably time to drop it.

Think about it. Paying $600 a year for full coverage on a car that’s only worth $4,000 doesn’t add up. You’d be better off saving that $600 in an emergency fund for any potential repairs. Just remember, you still have to maintain Georgia’s minimum liability coverage no matter what.

Why You Must Shop Around Annually

I’ll say it again: loyalty almost never pays in the insurance game. The single most effective thing you can do to lower your rate is to shop for new quotes at least once a year. A competitor might be hungry for business in your area and offer a deal your current insurer can’t touch.

Big life changes are also a perfect trigger to shop around. Did you move from a busy city like Savannah to a quieter suburb like Alpharetta? Your rate should drop. Did your credit score go up? That can lower your premium, too. Don’t wait for your insurance company to notice—go find a better price yourself.

When you start getting quotes, make sure you’re comparing apples to apples. Have these questions ready:

- “Are these coverage limits and deductibles the exact same as my current policy?”

- “Which discounts did you apply to this quote?”

- “Are there any extra fees or service charges I should know about?”

Taking control of your policy and making a habit of shopping around is how you beat rising costs and get the coverage you actually need at a fair price.

If you’ve already tightened up your policy and want another guaranteed way to save, don’t forget about completing a state-approved defensive driving course. It’s a small time investment for a guaranteed discount that can last for years. You can check out your options and find a class that works for you on our Defensive Driving course page.

Finding Affordable Insurance After a DUI in Georgia

Getting hit with a DUI conviction in Georgia creates a lot of problems, but one of the biggest headaches is what happens to your car insurance. Brace yourself, because your rates are about to jump—a lot. Insurers now see you as a high-risk driver, and they’ll price your policy accordingly.

Your first move will be getting an SR-22 certificate. This isn’t actually an insurance policy. It’s a form your insurance company files with the Georgia DDS to prove you have the minimum liability coverage the state requires. You can’t get your license reinstated after a DUI without it.

What to Know About the SR-22

Here’s the catch: not every insurance company will file an SR-22 for you. Your current provider might even drop you. You’ll need to shop around for an insurer that works with high-risk drivers. Get ready to make some calls and compare quotes.

Expect to pay those higher premiums for the next three to five years. Your main goal during this period is to keep your costs as low as possible while proving you’re a responsible driver again.

The single most important thing you can do is complete every court and state requirement as quickly as possible. That means finishing your DUI/Risk Reduction program—it’s the first real step toward getting your license back and, down the road, cleaning up your driving record.

When insurers see that you’ve completed these requirements, they know you’re taking this seriously. To get a full picture of the financial and legal challenges you’re facing, check out the consequences of a DUI in Georgia.

It’s a long road, but you can get through it. As long as you stay insured, keep your record clean from here on out, and meet all your legal obligations, you’ll slowly rebuild your good standing. Eventually, you’ll be able to qualify for standard, more affordable insurance again.

The best way to start is by enrolling in a state-approved DUI/Risk Reduction Program. Finishing this course is your ticket to putting this incident behind you and starting the process to lower your car insurance rates.

Your Questions About Lowering Car Insurance Answered

Let’s dig into some of the most common questions we hear from Georgia drivers about cutting their insurance costs. Here are some quick, straightforward answers to help you start saving.

How Often Should I Get New Insurance Quotes?

You should be shopping for new car insurance quotes at least once a year, especially right before your current policy is set to renew. Rates are always shifting, and what was a great deal twelve months ago might not be the most competitive option today.

It’s also a smart move to get fresh quotes anytime you have a major life change. This could be things like:

- Moving to a new zip code, like from a busy Atlanta neighborhood to a quieter suburb.

- Giving your credit score a significant boost.

- Adding or removing a driver or vehicle from your policy.

- Changing your daily commute.

Will a Defensive Driving Course Remove License Points?

Yes, it can, but there are some rules you need to know. In Georgia, you can ask the DDS to reduce your license point total by up to seven points once you complete a certified six-hour Defensive Driving Program.

The catch? You can only do this once every five years. This is a huge help for avoiding a potential license suspension, which would cause your insurance rates to spike even more.

Keep in mind, what your insurer really wants to see is you being proactive. Finishing a course shows them you’re a lower-risk driver, which often earns you a premium discount even if you don’t need points removed.

What Is the Fastest Way to Lower My Bill?

If you already have a clean driving record and have bundled your policies, there are two quick wins. The first is adjusting your policy itself. Simply raising your comprehensive and collision deductibles from $500 to $1,000 can create an immediate drop in your premium.

But for a guaranteed discount, your most direct route is taking a state-approved defensive driving course. This is a concrete step that gives you a verifiable certificate, qualifying you for a rate reduction of 5-15% that can last for up to three years.

Ready to take control of your insurance rates? At Georgia DUI Schools, completing a state-approved Defensive Driving course is one of the fastest ways to secure a guaranteed discount. Find a convenient online or in-person course today and start saving.

Powered by the Outrank tool